From Vulnerable to Certified: How a GCC Digital Wallet Protected 500K+ User Accounts

Key Takeaways:

- The regulators in the UAE are now requiring technical security evidence instead of the mere checkbox audits and basic compliance documents.

- Securing 500K+ users would require extensive API logic and microservices penetration testing to avoid fraud on a large scale.

- To ensure the GCC digital wallet is strong in terms of security, risk management should be considered as a continuous process and not a project.

- To overcome various regional regulations, a security partner must be knowledgeable of the technical and legal environment in the GCC.

- The contemporary GCC digital wallet security aspect relies on the detection of broken business logic and gaps in the authorization features that may not be identified by automated scanners.

Why Digital Wallet Security is a Critical Priority in the GCC

GCC digital wallet security has become the defining challenge for fintech leaders in a region where a single vulnerability can erase years of brand equity.

In the UAE’s hyper-growth environment, digital transactions are no longer just a convenience, they are a cornerstone of the economy.

These platforms have evolved from simple apps into critical financial infrastructure, managing billions of dirhams daily.

Market analyses of the GCC digital wallet landscape indicate that these systems are now so deeply embedded in commerce that their resilience is non-negotiable.

But growth brings problems. GCC digital wallet security isn’t optional anymore. When you’re managing hundreds of thousands of users in real-time, you’re also managing hundreds of thousands of potential attack vectors.

Your mobile apps, backend APIs, payment integrations each one is a door that needs locking.

Beyond the immediate damage to user trust, a security breach now functions as a direct regulatory trigger.

The Retail Payment Services and Card Schemes Regulation (RPSCS) is issued by the Central Bank of the UAE under its regulatory authority granted by Federal Decree Law No. 14 of 2018. It governs licensing and security obligations for payment service providers operating in the UAE mainland.

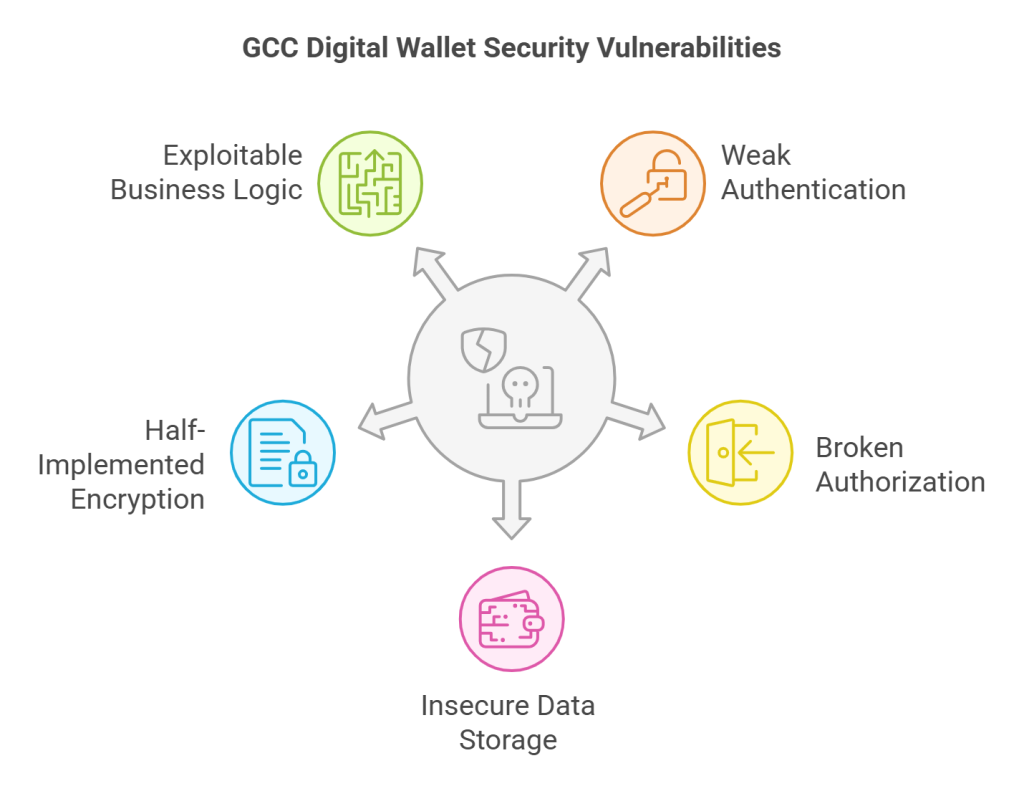

Common Security Gaps in GCC Digital Wallet Platforms

While expanding the attack surface in mobile wallet architectures, let’s break down where things typically go wrong. A modern digital wallet isn’t a single app, it’s an ecosystem.

You’ve got Android and iOS apps talking to backend APIs, microservices handling transactions, payment gateways processing money, and OTP providers managing authentication.

Every connection point may represent a potential vulnerability.

To maintain robust GCC digital wallet security, teams must look beyond the surface level.

Digital wallet vulnerability assessment GCC teams consistently find the same issues:

- Authentication that’s too weak

- APIs with broken authorization

- Mobile apps storing sensitive data insecurely

- Encryption that’s half-implemented

- Business logic that attackers can exploit

Broken session management remains a primary failure, allowing attackers to hijack active user journeys.

APIs frequently leak sensitive financial data by failing to verify authorization at the object level.

On the client side, mobile apps often store credentials in local storage like unlocked cash drawers. Furthermore, flawed business logic creates gaps in transaction workflows that bypass critical payment confirmations.

These aren’t theoretical problems; they are the systemic vulnerabilities identified in GCC digital wallet security assessments every single month.

Business & Regulatory Risks of Insecure Digital Wallets

What happens when security fails, account takeovers lead to fraudulent transactions. Fraudulent transactions trigger chargebacks.

Chargebacks mean financial losses. And in competitive markets like Dubai and the broader UAE, word spreads fast. Users abandon platforms that can’t protect their money.

One breach can cost you more customers than three years of marketing can win back. Beyond the immediate loss of capital, a failure in GCC digital wallet security erodes the foundational trust required for the region’s “cashless” ambitions to succeed.

Payment service providers in the UAE face serious compliance obligations. But here’s what catches people off guard: requirements aren’t uniform. Mainland UAE has different expectations than DIFC or ADGM. Each jurisdiction brings its own data protection and transaction security standards.

The CBUAE’s Retail Payment Services and Card Schemes Regulation, plus their Information Security Standards, spell out what’s expected. And regulators have gotten smart, they want evidence-based security testing, not just paperwork.

Checklist audits don’t prove anything. They just prove you completed a checklist.

The Challenge: Securing 500K+ User Accounts at Scale

One GCC digital wallet provider faced a dilemma that’s becoming common: they needed bulletproof secure digital wallet GCC operations, but couldn’t afford downtime. Not even minutes.

Over 500K+ users were actively transacting. The platform processed payments 24/7. Compliance deadlines were approaching. And traditional security approaches weren’t built for this scenario.

Do you know why traditional audits don’t work?

Those checkbox security audits? They miss the sophisticated stuff. An auditor can verify you have firewalls and encryption turned on, but they won’t find the business logic flaw that lets attackers manipulate transaction amounts.

They won’t catch the API endpoint that leaks user data when you send requests in a specific sequence.

Wattlecorp analyzed this pattern repeatedly in our compliance readiness and security assessment work for a leading digital bank. GCC financial institutions are waking up to a hard truth: conventional audits create false confidence.

What was required was comprehensive penetration testing for digital wallet protection, conducted by security researchers with an adversarial, attacker-focused mindset.

The Security Approach: Mobile Application Penetration Testing

Testing everything that matters, the security team adopted a systematic approach to GCC digital wallet security and rigorously assessed both Android and iOS applications while probing backend APIs for vulnerabilities.

They validated authentication mechanisms and authorization controls. They examined encryption implementations and storage security. They attacked transaction workflows and business logic.

This wasn’t automated scanning. Real security researchers reverse-engineered the mobile apps, analyzed how APIs communicated, and built custom exploits targeting this specific platform’s architecture.

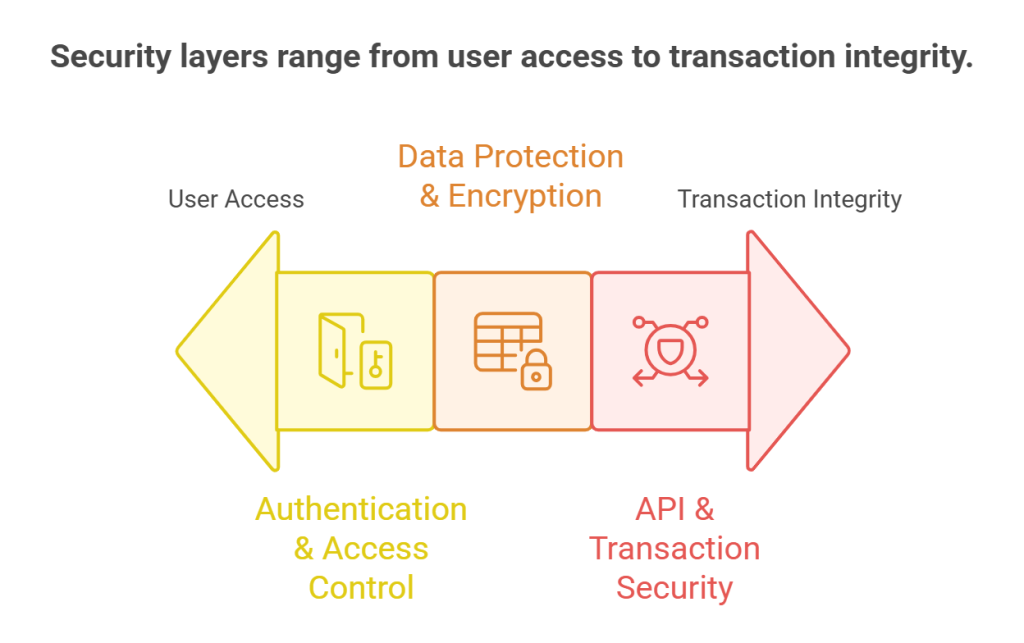

Three Critical Security Layers

1. Authentication & Access Control

Could multi-factor authentication be bypassed? How did the system handle session tokens? What happened when users switched roles or permissions? The GCC Digital wallet platform implemented MFA for high-risk authentication workflows and validated enforcement during penetration testing.

2. Data Protection & Encryption

Mobile payment cybersecurity demands encryption everywhere. But implementation matters more than intention. The team validated that sensitive data stayed encrypted on devices and during transmission. They looked for information leakage, those small gaps where data slips through.

3. API & Transaction Security

APIs are where business logic lives, and where clever attackers strike. Could someone access protected data without proper authorization? Would the system notice and stop automated attacks? Could transaction amounts be manipulated mid-process? Each vulnerability found meant one less avenue for fraud.

The Outcome: From Vulnerable to Certification-Ready

Security remediation reduces identified risk but does not guarantee elimination of future vulnerabilities. Transaction workflows got hardened against manipulation. Account takeover attacks that would’ve succeeded before now failed consistently.

Digital wallet security solutions aren’t about perfection, they are about making attacks economically unfeasible for criminals.

Also Read : Why Continuous Pentesting is Essential for Defending against Zero-Day Vulnerabilities in the UAE

Those 500,000+ user accounts? Protected. Regulators? More confident in the platform’s security posture. Fraud attempts? Dropping as attackers hit hardened defenses and moved to softer targets.

Customer trust improved measurably across Dubai and the wider UAE market. Retention metrics went up. User reviews mentioned security as a positive factor, not a concern.

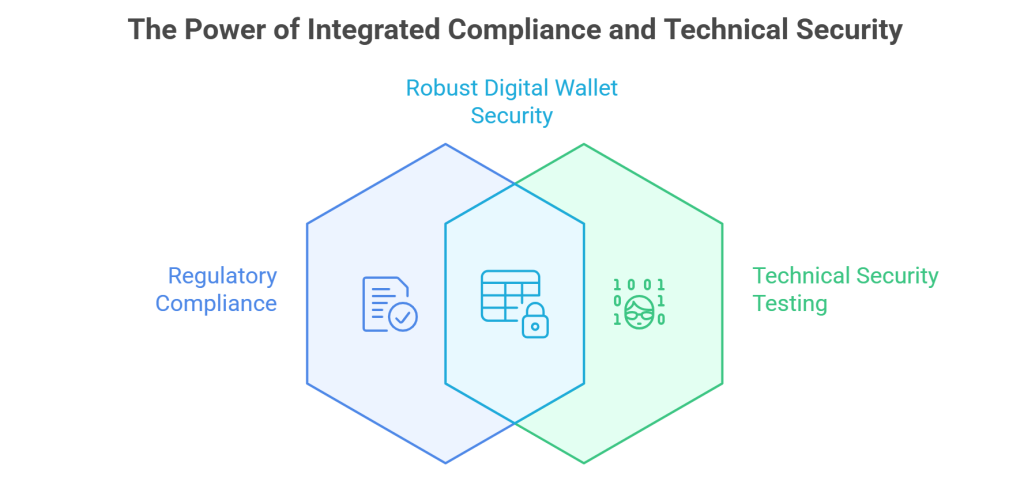

Compliance Alignment: Meeting UAE & GCC Payment Security Expectations

What regulators actually want is alignment with UAE payment regulations, specifically the CBUAE Retail Payment Services and Card Schemes Regulation and Information Security Standards, which require more than documentation.

Regulators want technical evidence and they want to see how security controls actually work under pressure.

The platform could now demonstrate, with testing artifacts and remediation proof, that they met requirements.

Industry best practice emphasizes combining compliance validation with technical security testing.

GCC digital wallet security frameworks need both regulatory checkbox completion and real-world threat mitigation. Otherwise, you’re compliant right up until the moment you’re breached.

Why Continuous Security Testing is Essential for Digital Wallets

Mobile malware gets more sophisticated yearly. Attackers reverse-engineer apps to extract API keys and encryption secrets. Credential stuffing campaigns use leaked passwords from other breaches. API abuse tools automate attacks at scale.

Digital wallet risk management can’t be a one-time project because the threat landscape won’t stay frozen.

Also Read : Why Both Manual and Automated Penetration Testing Are Essential for Continuous Security in UAE

To maintain strong GCC digital wallet security, risk management cannot be a one-time project because the threat landscape won’t stay frozen.

Mobile wallet security GCC best practices center on regular penetration testing by qualified specialists. Integrate security into your development lifecycle from day one.

Conduct continuous risk assessments and find vulnerabilities before attackers do. Stay ahead of compliance requirements instead of scrambling to catch up.

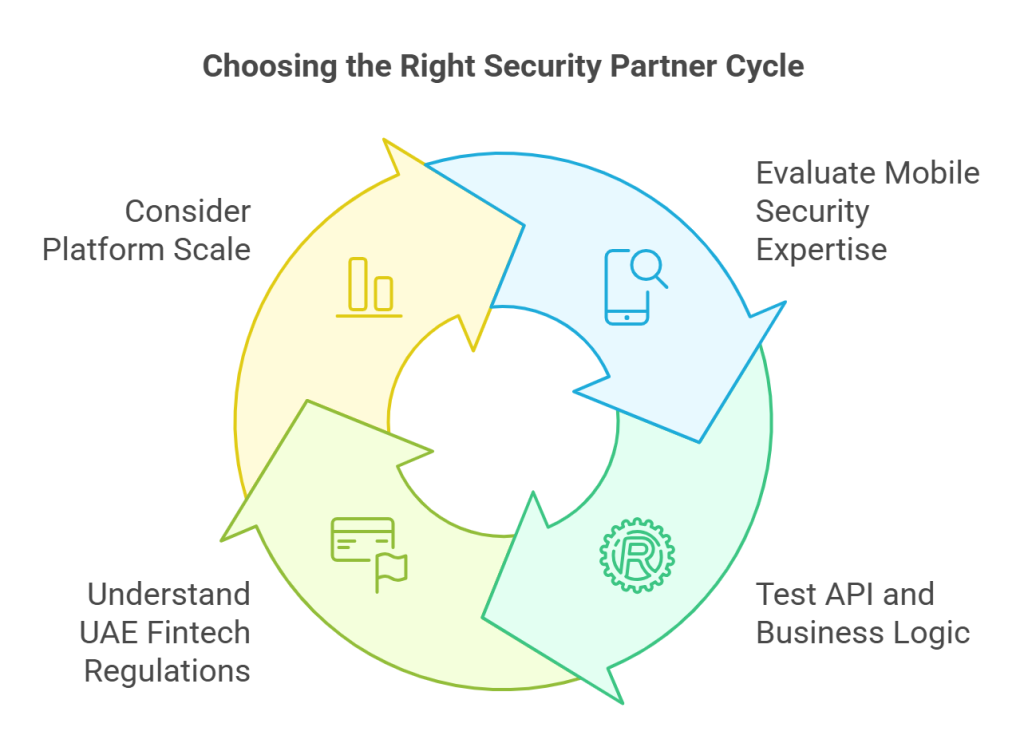

Choosing the Right Security Partner for Digital Wallet Protection

When you’re evaluating a VAPT company in Dubai, you need to look beyond the marketing. Do they understand mobile application security deeply? Can they test API and business logic, not just run scanners?

To ensure long-term GCC digital wallet security, ask yourself these critical questions:

Do they understand mobile application security deeply and they test API and business logic, not just run scanners?

Do they know UAE fintech regulations inside and out?

CBUAE regulations require strong authentication and robust information security controls under RPSCS and Information Security Standards, which means your partner must understand the nuances between mainland, DIFC, and ADGM requirements.

And critically: have they worked with high-scale platforms before? Testing a wallet with 500,000 users requires different expertise than testing a startup with 500.

These are the major things to consider when choosing the right security partner for GCC digital wallet security.

Certification is the Result of Strong Security Engineering

GCC digital wallet security isn’t a destination, it’s a practice. Certification happens when you’ve done the hard work of validating security under real-world conditions.

When regulators trust your platform, it’s because penetration testing proved your defenses work.

For digital wallets operating in the UAE and across the GCC, mobile application penetration testing isn’t optional infrastructure.

It’s the foundation that everything else builds on user trust, regulatory confidence, sustainable growth. Wattlecorp’s UAE operations specialize in exactly this kind of security work for regional fintech platforms. Our mobile application penetration testing services are built specifically for the challenges GCC digital wallet providers face.

GCC Digital Wallet Security FAQs

1. What are the top security threats for digital wallets in the GCC?

Account takeover through stolen credentials tops the list. API abuse exploiting weak authorization comes next. Mobile malware targeting UAE users is growing. Business logic flaws let attackers manipulate transactions. And insufficient encryption exposes financial data when it’s transmitted or stored. Each threat requires different defensive approaches.

2. How do digital wallets protect user data with multi-factor authentication?

Multi-factor authentication stacks verification layers. Something you know (password) with something you have (phone for OTP) and sometimes something you are (fingerprint or face scan). Even if attackers steal your password, they’d still need your physical device and potentially your biometrics. That combination makes account takeover exponentially harder.

3. Why is regular penetration testing critical for mobile wallets?

Your wallet gets new features and attackers develop new techniques. Code changes introduce new bugs. Regular testing catches vulnerabilities before criminals exploit them. In the UAE and GCC, where digital wallet adoption is accelerating, the threat landscape shifts constantly. Yesterday’s secure configuration might have today’s exploitable weakness.

4. What compliance requirements exist in the UAE for digital wallet providers?

UAE digital wallet providers must satisfy CBUAE regulations, specifically the Retail Payment Services and Card Schemes Regulation and Information Security Standards. But it gets complicated: Mainland UAE, DIFC, and ADGM each have distinct frameworks for data protection and transaction security. Your compliance requirements depend on where you’re operating and which regulators have jurisdiction.

5. How did penetration testing help protect 500K+ digital wallet accounts?

Penetration testing found critical vulnerabilities before attackers could weaponize them. It validated that security controls actually worked under attack conditions, not just in theory. Authentication and encryption got strengthened based on what testing revealed. Transaction logic got hardened against manipulation. And the platform generated technical evidence for regulatory compliance, all of which collectively protected every user account from takeover and fraud.

AI-Powered Cyberattacks in India 2026: What CISOs Need to Know Now

AI-Powered Cyberattacks in India 2026: What CISOs Need to Know Now

Key Takeaways: Generative AI has sharply accelerated the attacker’s advantage by making phishing, reconnaissance, and exploit preparation faster and easier to scale. Being a CISO in 2026 means making real-time threat decisions at board level, that’s a different job from what most security leaders are trained for, and the skill gap is already showing. CERT-In’s […]

ISO 27001 Internal Audit for Saudi Companies: Preparing Evidence Before Certification

ISO 27001 Internal Audit for Saudi Companies: Preparing Evidence Before Certification

Key Takeaways: An ISO 27001 internal audit helps Saudi companies validate whether their Information Security Management System is implemented, not just documented. Certification auditors do not only review policies. They check risk registers, control ownership, access reviews, incident records, supplier reviews, audit trails, management review minutes, and corrective action evidence. For Saudi companies, ISO 27001 […]

Proactive Threat Hunting for UAE Enterprises: Finding Attackers Before They Strike

Proactive Threat Hunting for UAE Enterprises: Finding Attackers Before They Strike

Key Takeaways: Proactive threat hunting is not the same as traditional monitoring. Monitoring waits for the alerts, while threat hunting actively searches for signs of attacker behaviour that may not trigger automated detection. For UAE enterprises, threat hunting is becoming more important because attacks are shifting from simple malware to credential abuse, ransomware preparation, cloud […]

CERT-IN Empanelled VAPT: Why Indian Companies Should Choose CERT-IN Approved Firms in 2026

CERT-IN Empanelled VAPT: Why Indian Companies Should Choose CERT-IN Approved Firms in 2026

Key Takeaways: Running a VAPT with a CERT-In empanelled firm means your security testing is backed by a standard that regulators and enterprise clients in India actually recognize, not just a vendor promise. When sensitive data and critical systems are involved, a CERT-In empanelled VAPT provider gives Indian companies compliance readiness they can demonstrate, not […]

SOC 2 Type I vs Type II Timeline: How Long UAE Companies Actually Need

SOC 2 Type I vs Type II Timeline: How Long UAE Companies Actually Need

Key Takeaways: SOC 2 Type I vs Type II timelines differ and it is mostly based on audit depth. Type I checks if controls are well-designed at a given point in time. Type II goes a step further and it proves those controls worked consistently over a defined period. For UAE SaaS companies, Type I […]

AI Security Testing for US SaaS Platforms: NIST AI RMF and What 2026 Standards Require

AI Security Testing for US SaaS Platforms: NIST AI RMF and What 2026 Standards Require

Key Takeaways: AI security testing for SaaS platforms isn’t just a technical upgrade from traditional app security. It’s a completely different job. You’re not running a scan on code, you’re stress-testing a model to see how it breaks when someone is actively trying to make it fail. NIST AI RMF isn’t law yet, but your […]